Student Loan Repayment 2026: New Programs & Strategies to Cut Your Monthly Burden by 10%

Anúncios

The landscape of student loan repayment is continuously shifting, and as we approach 2026, borrowers are keenly anticipating new programs and strategies that could offer significant relief. For many, the weight of student debt can feel overwhelming, impacting life choices from career paths to homeownership. The good news is that the federal government, alongside various private initiatives, is consistently working to refine and introduce options designed to make repayment more manageable. This comprehensive guide delves into the 2026 outlook for student loan repayment, exploring new programs, enhanced existing ones, and actionable strategies to help you reduce your monthly burden by at least 10%.

Anúncios

Understanding the nuances of student loan repayment is crucial for effective financial planning. With billions of dollars in outstanding student debt, the economic and personal implications are vast. This article aims to demystify the complexities, providing a clear roadmap for borrowers to navigate their options, optimize their repayment plans, and ultimately achieve financial freedom. Whether you’re a recent graduate, a seasoned professional, or someone returning to education, the information presented here will empower you to make informed decisions about your student loans.

The Evolving Landscape of Student Loan Repayment: What to Expect in 2026

The past few years have seen significant changes in student loan policies, from payment pauses to the introduction of new income-driven repayment (IDR) plans. These shifts underscore a commitment to addressing the student debt crisis. As we look towards 2026, several key trends and potential policy adjustments are on the horizon that could dramatically impact student loan repayment for millions of Americans.

Anúncios

Federal Programs: A Focus on Affordability and Accessibility

The federal government remains the primary source of student loans and, consequently, the main driver of repayment policy. Expect continued emphasis on making federal student loan repayment more affordable and accessible. This includes potential further enhancements to IDR plans, which tailor monthly payments to a borrower’s income and family size. The goal is to ensure that no borrower has to choose between making their loan payments and meeting basic living expenses.

The SAVE Plan: A Game Changer for Many Borrowers

The Saving on a Valuable Education (SAVE) Plan, which began rolling out in 2023, is poised to be a cornerstone of student loan repayment in 2026. This plan offers some of the most generous terms ever seen for federal student loan borrowers. Key features include:

- Lower Monthly Payments: For undergraduate loans, payments are calculated at 5% of discretionary income, down from 10-15% in older IDR plans. This alone can lead to a significant reduction in monthly outlays.

- Interest Subsidy: A crucial benefit of the SAVE Plan is that if your calculated payment doesn’t cover the monthly interest, the government covers the remaining interest. This prevents your loan balance from growing due to unpaid interest, a common frustration for borrowers on other IDR plans.

- Shorter Repayment Periods for Smaller Balances: Borrowers with original loan balances of $12,000 or less could see forgiveness after just 10 years of payments. This is a substantial reduction from the standard 20 or 25 years for other IDR plans.

- Expanded Definition of Discretionary Income: The SAVE Plan increases the amount of income protected from repayment calculations, meaning more of your income is considered non-discretionary. This further lowers the amount used to calculate your payment.

By 2026, the SAVE Plan is expected to be fully implemented and widely adopted. If you haven’t already, understanding its provisions and how it can benefit you is paramount. Switching to the SAVE Plan could be the single most impactful strategy to reduce your monthly student loan burden.

Potential for Further Policy Adjustments

While the SAVE Plan is a major development, the political and economic environment could lead to further policy adjustments. These might include:

- Streamlined IDR Enrollment: Efforts to simplify the annual recertification process for IDR plans could be implemented, making it easier for borrowers to stay on track and avoid payment shocks.

- Targeted Forgiveness Programs: Beyond existing programs like Public Service Loan Forgiveness (PSLF), there might be discussions or proposals for new, targeted forgiveness initiatives based on specific professions, economic hardship, or loan types.

- Improvements to Loan Servicing: The Department of Education continues to work on improving the student loan servicing experience, aiming for greater transparency, better communication, and more efficient processing of applications and inquiries.

Staying informed about these potential changes will be vital as 2026 approaches. Reliable sources like the Department of Education’s student aid website are your best resource for the most up-to-date information.

Strategic Approaches to Reduce Your Monthly Student Loan Burden by 10% or More

Achieving a 10% reduction in your monthly student loan payment is an achievable goal for most borrowers, especially with the programs and strategies available in 2026. Here’s how you can do it:

1. Re-evaluate Your Federal Loan Repayment Plan

This is often the most impactful step. Many borrowers are on the Standard Repayment Plan, which, while predictable, doesn’t account for income fluctuations. Exploring IDR plans is crucial.

The SAVE Plan: Your First Stop

As discussed, the SAVE Plan is likely your best bet for reducing payments. If you are currently on a different IDR plan (PAYE, IBR, ICR), compare its terms to SAVE. For many, switching to SAVE will result in lower monthly payments, especially if you have a lower income relative to your debt. The interest subsidy alone can save you hundreds, if not thousands, of dollars over the life of the loan by preventing balance growth.

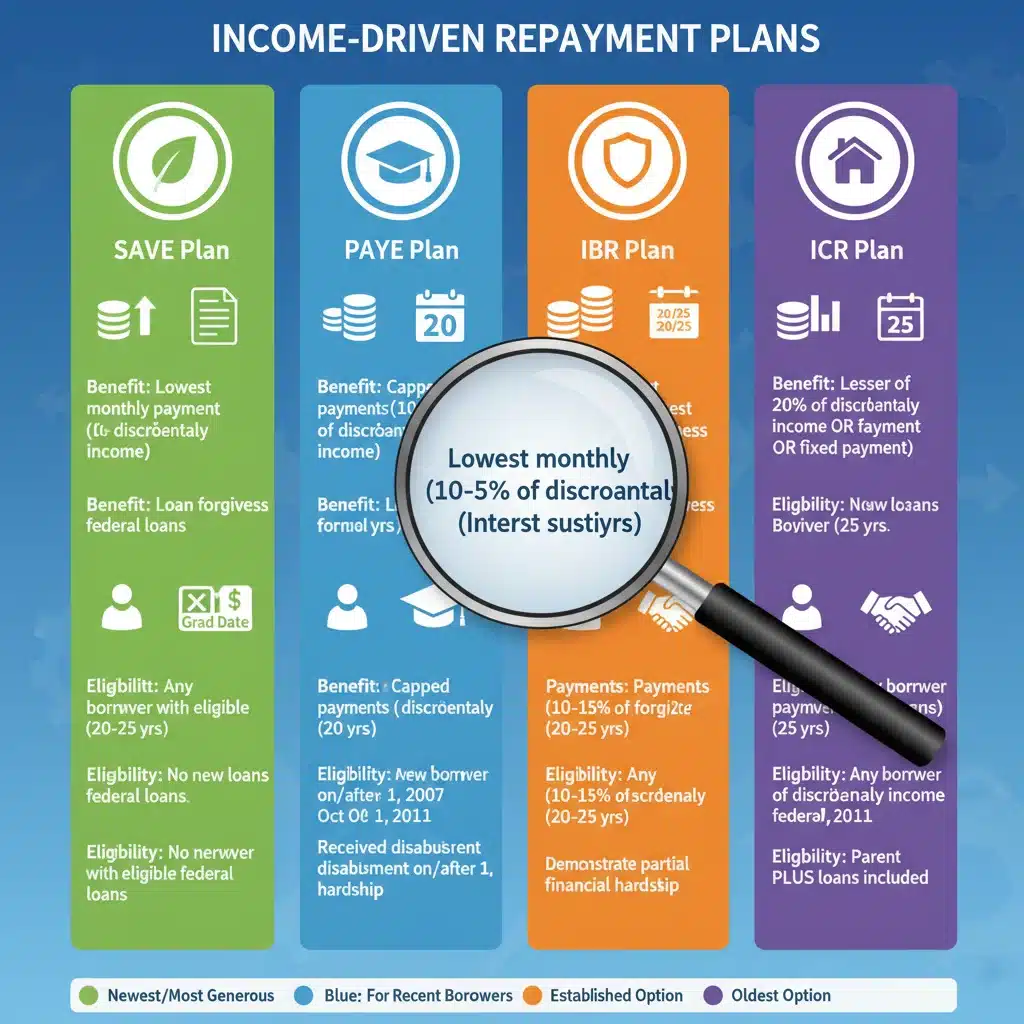

Other IDR Options (PAYE, IBR, ICR)

While SAVE is often the most beneficial, it’s worth understanding the others in case your specific circumstances make one of them more advantageous (though this is becoming less common with SAVE’s enhancements):

- Pay As You Earn (PAYE): Payments are generally 10% of discretionary income, capped at the 10-year Standard Repayment Plan amount. Loan forgiveness after 20 years.

- Income-Based Repayment (IBR): Payments are 10% or 15% of discretionary income, depending on when you took out your loans, capped at the 10-year Standard Repayment Plan amount. Loan forgiveness after 20 or 25 years.

- Income-Contingent Repayment (ICR): Payments are the lesser of 20% of discretionary income or what you’d pay on a fixed 12-year plan, adjusted for income. Loan forgiveness after 25 years.

Use the Federal Student Aid Loan Simulator to compare how your payments would look under each plan. This tool is invaluable for making an informed decision.

2. Explore Public Service Loan Forgiveness (PSLF)

If you work for a government agency (federal, state, local, or tribal) or a qualifying non-profit organization, PSLF could be a game-changer. After 120 qualifying monthly payments (10 years) while working full-time for a qualifying employer and on a qualifying repayment plan (typically an IDR plan), your remaining federal direct loan balance can be forgiven tax-free. The PSLF program has seen significant improvements, making it more accessible to borrowers who previously struggled with its strict requirements.

Key PSLF Considerations for 2026:

- Eligible Employers: Ensure your employer qualifies. This generally includes most government organizations and 501(c)(3) non-profits.

- Eligible Loans: Only Direct Loans qualify. If you have FFEL or Perkins loans, you may need to consolidate them into a Direct Consolidation Loan to become eligible.

- Eligible Payment Plan: You must be on an income-driven repayment plan.

- Full-Time Employment: Generally, working at least 30 hours per week for one or more qualifying employers.

Even if you’re only a few years into public service, understanding PSLF now can help you structure your repayment to maximize its benefits. The monthly payment reduction under an IDR plan, combined with future forgiveness, can lead to substantial savings.

3. Consider Student Loan Refinancing (for Private Loans or Specific Federal Loan Situations)

Refinancing involves taking out a new loan, usually from a private lender, to pay off existing student loans. This can be beneficial if you have excellent credit and a stable income, as you might qualify for a lower interest rate, which in turn reduces your monthly payment and the total amount paid over time.

When Refinancing Makes Sense:

- Private Student Loans: Refinancing private loans is often a good strategy as they typically lack the federal protections (IDR plans, forgiveness programs) that federal loans offer. A lower interest rate on a private loan can lead to significant savings.

- High-Interest Federal Loans (with caution): While generally not recommended due to the loss of federal protections, if you have very high-interest federal loans, a strong financial position, and absolutely no need for IDR plans or forgiveness, refinancing could lower your rate. However, proceed with extreme caution and fully understand what you’re giving up.

- Shorter Repayment Term: If your goal is to pay off loans faster, you might refinance to a shorter term with a slightly lower rate, though your monthly payment might increase. Conversely, extending the term could lower your monthly payment, but you’ll pay more interest over time.

The competitive private lending market in 2026 means there will likely be attractive refinancing options. Shop around, compare rates from multiple lenders, and read the fine print carefully.

4. Optimize Your Budget and Increase Payments (If Possible)

While the goal is to reduce your monthly burden, for those who can afford it, strategically increasing payments (even slightly) can lead to long-term savings. However, if your primary goal is to lower your current monthly payment, this strategy might seem counterintuitive. The key here is optimization.

- Identify Savings: Go through your budget with a fine-tooth comb. Can you cut discretionary spending by 5-10%? Even small savings on dining out, entertainment, or subscriptions can add up.

- Additional Income: Explore side hustles or temporary gigs. Even an extra $50-$100 per month can make a difference.

- Understand the Trade-off: If you’re on an IDR plan and your payment is low, any extra payment you make goes directly to the principal or interest that the government isn’t subsidizing, helping you pay off the loan faster or reducing the amount forgiven at the end.

This strategy is about finding the sweet spot where you can comfortably meet your obligations while potentially accelerating your path to debt freedom, or at the very least, ensuring your loans don’t grow due to interest.

5. Leverage Tax Benefits

Don’t forget about the student loan interest deduction. You can deduct the amount of interest you paid during the year on a qualified student loan, up to $2,500, or the amount of interest you actually paid, whichever is less. This deduction can reduce your taxable income, potentially leading to a lower tax bill or a larger refund, which indirectly helps your overall financial situation and can free up funds for other financial goals or even to put towards your loans.

Key Points for 2026 Tax Season:

- Eligibility: The deduction is available for both federal and private student loans.

- Income Limitations: There are income phase-outs for this deduction, so check the IRS guidelines for 2026 to see if you qualify based on your modified adjusted gross income (MAGI).

- Form 1098-E: Your loan servicer should send you Form 1098-E if you paid at least $600 in interest during the year. Keep this form for your tax records.

6. Understand and Utilize Deferment and Forbearance (as a Last Resort)

While not a strategy to *reduce* your monthly payment in the long term, deferment and forbearance allow you to temporarily postpone payments. These options should be considered as a last resort for financial hardship, as interest may accrue during these periods, increasing your total loan cost.

When to Consider Deferment or Forbearance:

- Unemployment: If you lose your job or experience a significant reduction in income.

- Economic Hardship: If you are struggling to meet essential living expenses.

- Medical Leave: If you need to take time off work for medical reasons.

Always contact your loan servicer immediately if you anticipate difficulty making payments. They can explain your options and help you apply for deferment or forbearance if appropriate. Remember, defaulting on your loans has severe long-term consequences for your credit and financial health.

Proactive Steps for 2026 and Beyond

Successfully navigating student loan repayment requires a proactive and informed approach. Here are some key steps you should take as we move into 2026:

Stay Informed and Monitor Policy Changes

The student loan landscape is dynamic. Regularly check official sources like the U.S. Department of Education’s StudentAid.gov website for the latest updates on programs, eligibility requirements, and deadlines. Subscribe to newsletters from reputable financial aid organizations.

Know Your Loan Servicer

Your loan servicer is your primary point of contact for all repayment-related questions. Know who they are, how to contact them, and keep your contact information updated. Don’t hesitate to reach out to them if you have questions about your payment plan, eligibility for new programs, or if you’re experiencing financial difficulty.

Maintain Accurate Records

Keep meticulous records of all communications with your loan servicer, payment confirmations, and any applications you submit for IDR plans or forgiveness programs. This documentation can be invaluable if discrepancies arise.

Regularly Re-evaluate Your Financial Situation

Your income, family size, and financial goals can change over time. It’s wise to review your student loan repayment plan annually, especially if you’re on an IDR plan, to ensure it still aligns with your current circumstances and offers the most advantageous terms. This annual review can also ensure you re-certify your income on time to avoid payment increases.

Seek Professional Advice (When Needed)

If your student loan situation is particularly complex, or if you’re struggling to understand your options, consider consulting with a non-profit credit counselor or a financial advisor specializing in student debt. Be wary of companies that promise quick fixes or charge upfront fees for services that are available for free through your loan servicer or the Department of Education.

Case Studies: Real-World Impact of New Programs

To illustrate the potential impact of these strategies, let’s consider a couple of hypothetical scenarios for 2026:

Case Study 1: The Recent Graduate

Meet Sarah: Sarah graduated in 2025 with $35,000 in federal student loans at an average interest rate of 6%. Her initial Standard Repayment Plan payment is around $389/month. She secured a job earning $40,000 annually. Under the SAVE Plan, her discretionary income is calculated based on 225% of the federal poverty line. For a single individual in 2026, let’s assume the poverty line is around $15,000, making 225% approximately $33,750. Her discretionary income would be $40,000 – $33,750 = $6,250. Her monthly payment would be 5% of this, divided by 12, resulting in approximately $26/month.

Impact: Sarah’s monthly payment drops from $389 to $26, a reduction of over 90%! The government covers the remaining interest, preventing her balance from growing. After 10 years, her remaining balance will be forgiven.

Case Study 2: The Mid-Career Professional

Meet David: David has $80,000 in federal student loans from undergraduate and graduate studies, with an average interest rate of 5.5%. He’s been on an IBR plan for years, paying $450/month based on his $70,000 salary. He’s married with one child. Under the SAVE Plan, for a family of three, 225% of the poverty line (let’s assume around $25,000) would be $56,250. His discretionary income would be $70,000 – $56,250 = $13,750. His monthly payment would be 5% of this, divided by 12, resulting in approximately $57/month.

Impact: David’s monthly payment drops from $450 to $57, an 87% reduction! Again, the interest subsidy is crucial here, stopping the balance from growing. He still has 15 years until potential forgiveness, but his monthly cash flow significantly improves.

These examples highlight the transformative potential of the SAVE Plan. While individual circumstances vary, the opportunity to significantly reduce monthly student loan payments in 2026 is real and accessible for many.

Conclusion: Taking Control of Your Student Loan Repayment in 2026

The 2026 outlook for student loan repayment offers a blend of continuity and innovation, with a strong emphasis on borrower support. The introduction and full implementation of programs like the SAVE Plan, coupled with ongoing efforts to streamline existing options, present a powerful opportunity for borrowers to gain better control over their finances. By proactively engaging with your loan servicer, understanding your eligibility for various repayment plans and forgiveness programs, and making informed decisions, you can significantly reduce your monthly student loan burden – potentially by 10% or even more.

Remember, your student debt journey is unique. What works for one borrower may not be the best solution for another. Take the time to assess your individual situation, utilize the available resources, and don’t hesitate to seek guidance when needed. With the right strategies and a commitment to staying informed, 2026 can be the year you take a decisive step towards managing your student loans more effectively and achieving greater financial stability.

By focusing on these strategies and staying abreast of policy developments, you can transform your approach to student loan repayment, turning what might feel like a daunting obligation into a manageable part of your financial life. The goal isn’t just to make payments, but to make smart payments that align with your broader financial goals and well-being.