Smart Debt Consolidation 2026: Reduce Loan Interest by 10% or More

Anúncios

Smart Debt Consolidation in 2026: How to Reduce Interest Payments by Up to 10% on Existing Loans

Anúncios

In an ever-evolving financial landscape, managing debt effectively is paramount for achieving financial stability and growth. As we move into 2026, the strategies for debt consolidation 2026 are becoming more sophisticated, offering innovative ways to reduce interest payments and simplify your financial life. This comprehensive guide will delve into the best practices for smart debt consolidation 2026, focusing on how you can potentially slash your interest rates by 10% or even more on existing loans. We’ll explore various methods, discuss their pros and cons, and provide actionable advice to help you make informed decisions.

Understanding Debt Consolidation: A Modern Approach for 2026

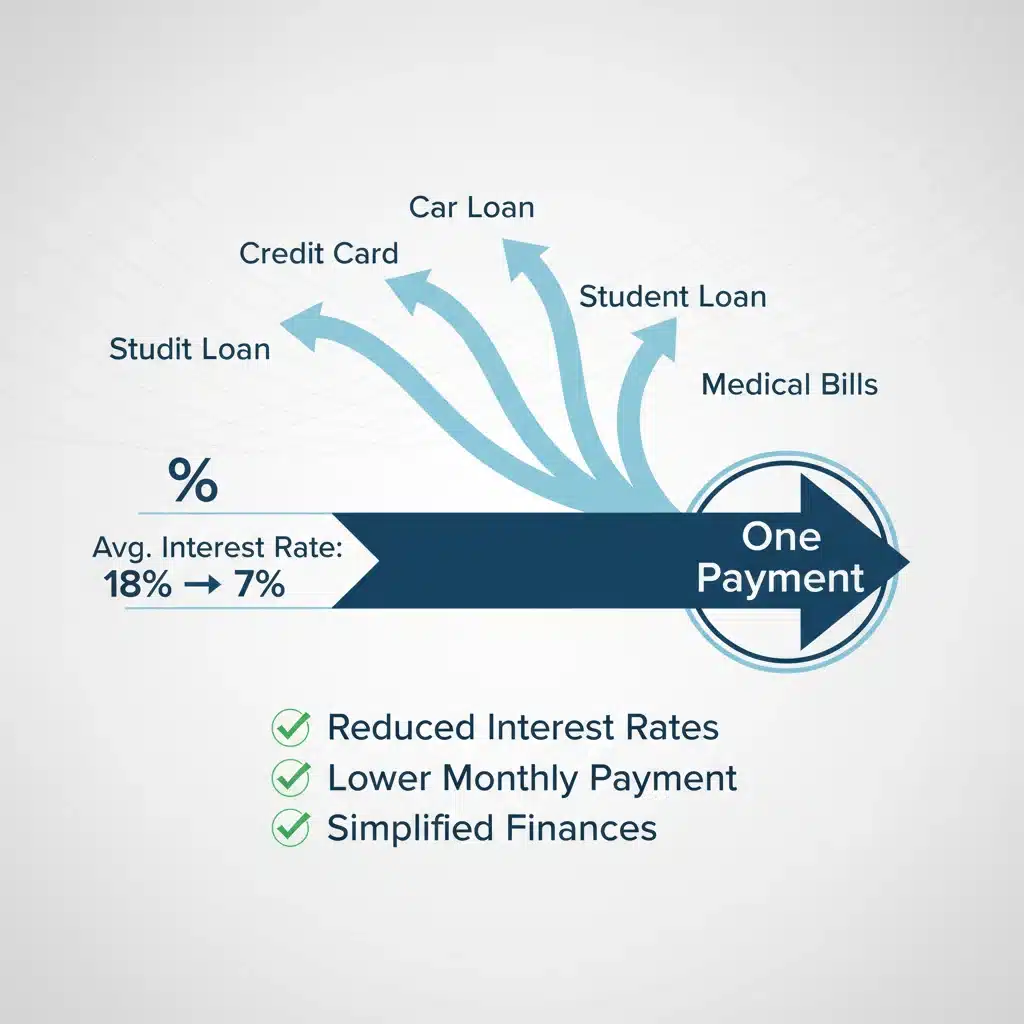

Debt consolidation isn’t a new concept, but its application and effectiveness are continually refined. At its core, debt consolidation involves combining multiple high-interest debts into a single, more manageable loan, ideally with a lower interest rate. This approach simplifies your monthly payments, reduces the total interest paid over time, and can significantly improve your credit score if managed correctly. For 2026, the emphasis is on leveraging technology, understanding market trends, and choosing the right financial products to maximize savings.

Anúncios

Why Consider Debt Consolidation in 2026?

- Lower Interest Rates: The primary appeal of debt consolidation 2026 is the potential to secure a lower overall interest rate. This translates directly into significant savings over the life of your loans.

- Simplified Payments: Instead of juggling multiple due dates and creditors, you’ll have one consolidated payment, making budgeting and financial management much easier.

- Improved Financial Health: By reducing interest payments, more of your money goes towards the principal, accelerating your debt repayment journey. This can free up cash flow for other financial goals, such as saving or investing.

- Credit Score Boost: Consistently making on-time payments on a consolidated loan can positively impact your credit score, opening doors to better financial products in the future.

- Reduced Stress: The psychological burden of multiple debts can be immense. Consolidating can provide a sense of control and relief, allowing you to focus on your financial future with less anxiety.

Key Strategies for Smart Debt Consolidation 2026

As you plan your debt consolidation 2026 strategy, it’s crucial to understand the different avenues available. Each method has unique characteristics, and the best choice for you will depend on your specific financial situation, credit score, and debt profile.

1. Balance Transfer Credit Cards: A Short-Term Solution

Balance transfer credit cards can be an excellent option for individuals with good credit and manageable debt, especially if they can pay off the transferred amount within the promotional 0% APR period. Many cards offer introductory periods ranging from 12 to 21 months with no interest on transferred balances. This can be a powerful tool for debt consolidation 2026 if used strategically.

Pros:

- 0% APR Period: This is the biggest advantage, allowing you to pay down principal without accruing interest for a significant period.

- Quick Setup: The application process is generally straightforward and fast.

- Reduced Monthly Payments: With no interest, your entire payment goes towards reducing your debt.

Cons:

- Balance Transfer Fees: Most cards charge a fee, typically 3-5% of the transferred amount.

- Expiration of 0% APR: If you don’t pay off the balance before the promotional period ends, remaining balances will be subject to a much higher standard APR, often negating any initial savings.

- Credit Score Requirement: You generally need a good to excellent credit score to qualify for the best balance transfer offers.

- Credit Limit Restrictions: The credit limit offered might not be sufficient to consolidate all your debts.

Pro Tip for 2026: Look for cards with the longest 0% APR periods and the lowest balance transfer fees. Create a strict repayment plan to ensure the debt is cleared before interest kicks in. This is a critical component of successful debt consolidation 2026.

2. Personal Loans for Debt Consolidation: A Flexible Option

Personal loans are a popular choice for debt consolidation 2026 because they offer a fixed interest rate and a fixed repayment schedule. This predictability makes budgeting easier and ensures you know exactly when your debt will be paid off. These loans are typically unsecured, meaning you don’t need to put up collateral.

Pros:

- Fixed Interest Rates: Your interest rate won’t change, providing stability and predictability.

- Predictable Payments: You’ll have a consistent monthly payment amount, making financial planning simpler.

- Potentially Lower Interest Rates: If you have good credit, you may qualify for a lower interest rate than what you’re currently paying on credit cards or other high-interest debts.

- One Monthly Payment: All your consolidated debts are rolled into a single loan, simplifying your finances.

- No Collateral Required: Most personal loans are unsecured.

Cons:

- Credit Score Impact: A new loan inquiry can temporarily lower your credit score.

- Approval Requirements: Lenders will review your credit history, income, and debt-to-income ratio.

- Origination Fees: Some lenders charge an origination fee, typically 1-5% of the loan amount, which can reduce the total amount you receive.

- Longer Repayment Periods: While lower monthly payments are appealing, a longer repayment period can mean paying more interest overall, even with a lower rate, if not managed carefully.

Pro Tip for 2026: Shop around with multiple lenders to compare interest rates, fees, and terms. Online lenders, traditional banks, and credit unions all offer personal loans. Focus on obtaining the lowest APR and a manageable repayment term to optimize your debt consolidation 2026 efforts.

3. Home Equity Loans or Lines of Credit (HELOCs): Leveraging Your Assets

For homeowners, a home equity loan or HELOC can be a powerful tool for debt consolidation 2026, as they typically offer much lower interest rates than unsecured loans due to being secured by your home. A home equity loan provides a lump sum, while a HELOC offers a revolving line of credit.

Pros:

- Lowest Interest Rates: Because your home serves as collateral, these loans often come with the lowest interest rates available.

- Tax Deductible Interest: In some cases, the interest on home equity loans can be tax-deductible (consult a tax professional).

- Large Loan Amounts: You can typically borrow a substantial amount, allowing you to consolidate significant debt.

Cons:

- Risk of Foreclosure: If you default on payments, you risk losing your home, which is a significant drawback.

- Closing Costs: These loans come with closing costs, similar to a mortgage, which can add to the overall expense.

- Variable Interest Rates (HELOCs): While initially low, HELOC rates can fluctuate, potentially increasing your payments over time.

- Equity Requirement: You need sufficient equity in your home to qualify.

Pro Tip for 2026: Carefully weigh the risks and benefits. Only consider this option if you are confident in your ability to make consistent payments and have a stable financial outlook. This is a vital consideration for effective debt consolidation 2026.

4. Debt Management Plans (DMPs) through Credit Counseling Agencies

If your credit score isn’t strong enough for a balance transfer or personal loan, or if you’re struggling to manage your debts, a Debt Management Plan (DMP) offered by non-profit credit counseling agencies can be a viable option for debt consolidation 2026. In a DMP, the agency negotiates with your creditors to lower interest rates, waive fees, and create a single, affordable monthly payment.

Pros:

- Lower Interest Rates: Creditors often agree to reduce interest rates for consumers in DMPs.

- Waived Fees: Late fees and over-limit fees might be waived.

- Simplified Payments: You make one payment to the agency, which then distributes funds to your creditors.

- Improved Financial Education: Counseling agencies provide valuable financial literacy and budgeting advice.

- No New Loan: You’re not taking on new debt; you’re simply restructuring existing debt.

Cons:

- Impact on Credit Score: While DMPs can help in the long run, the initial notation on your credit report can be negative.

- Account Closures: Your credit card accounts will typically be closed, which can temporarily affect your credit utilization.

- Fees: Agencies may charge a setup fee and a monthly administrative fee.

- Not All Debts Included: Secured debts, student loans, and tax debts are usually not included in DMPs.

Pro Tip for 2026: Choose a reputable, non-profit credit counseling agency accredited by organizations like the National Foundation for Credit Counseling (NFCC). Verify their credentials and ensure they offer transparent fee structures. This is a responsible approach to debt consolidation 2026 when other options are limited.

How to Achieve a 10% or More Interest Rate Reduction with Debt Consolidation 2026

The goal of debt consolidation 2026 is not just to simplify payments, but to significantly reduce the cost of your debt. Achieving a 10% or more reduction in interest payments is often attainable with careful planning and execution.

1. Assess Your Current Debt Landscape

Before you embark on any consolidation strategy, gather all your debt information: creditor names, outstanding balances, current interest rates, and minimum monthly payments. Calculate your weighted average interest rate across all your debts. This baseline will help you measure the success of your debt consolidation 2026 efforts.

2. Improve Your Credit Score

A higher credit score unlocks better interest rates. Before applying for new loans or balance transfer cards, take steps to improve your credit: pay bills on time, reduce credit utilization, and dispute any errors on your credit report. Even a slight improvement can lead to significant savings in interest. This is a foundational step for impactful debt consolidation 2026.

3. Compare Offers Diligently

Don’t jump at the first offer you receive. Request quotes from multiple lenders for personal loans, research various balance transfer cards, and explore options with credit counseling agencies. Pay close attention to APRs, fees (origination fees, balance transfer fees), and repayment terms. Use online calculators to estimate your total savings with different scenarios.

4. Negotiate with Creditors (Even Before Consolidating)

Sometimes, simply calling your current creditors and explaining your situation can lead to lower interest rates or more favorable terms, especially if you have a good payment history. This proactive step can sometimes be a form of ‘mini-consolidation’ in itself or set you up for better terms when you do consolidate, enhancing your debt consolidation 2026 strategy.

5. Create a Solid Repayment Plan

Once you’ve consolidated, the work isn’t over. Develop a strict budget and a clear repayment plan. Stick to your new, consolidated monthly payment. Avoid taking on new debt. The goal is to eliminate debt, not just shuffle it around. This commitment is vital for the long-term success of debt consolidation 2026.

6. Consider a Shorter Repayment Term (If Affordable)

While a longer repayment term might offer lower monthly payments, it often means paying more interest over time. If your budget allows, opt for the shortest repayment term possible with a manageable monthly payment. This accelerates your debt-free journey and maximizes your interest savings, a key aim of debt consolidation 2026.

Potential Pitfalls to Avoid in Debt Consolidation 2026

While debt consolidation 2026 offers numerous benefits, it’s not without its risks. Being aware of these potential pitfalls can help you navigate the process successfully.

1. Accumulating New Debt

One of the biggest dangers is consolidating debt only to rack up new charges on your now-empty credit cards. This can lead to an even worse financial situation. Discipline is key.

2. High Fees

Some consolidation products come with significant fees, such as origination fees on personal loans or balance transfer fees on credit cards. These fees can eat into your savings if not accounted for.

3. Longer Repayment Periods with Minimal Savings

Be wary of consolidation loans that offer very low monthly payments but stretch repayment over an excessively long period. While the monthly burden might feel lighter, you could end up paying more in total interest, even with a lower APR. Always calculate the total cost of the loan.

4. Predatory Lenders

Be cautious of lenders offering ‘guaranteed’ approval or extremely low rates without proper credit checks. These could be predatory loans with hidden fees or unfavorable terms. Always research lenders thoroughly.

5. Ignoring the Root Cause of Debt

Debt consolidation 2026 is a tool to manage debt, not a cure for overspending or poor financial habits. Unless you address the underlying reasons for your debt, you risk falling back into the same patterns. Financial education and budgeting are crucial alongside consolidation.

The Future of Debt Consolidation: Trends for 2026 and Beyond

The financial technology (FinTech) sector continues to innovate, bringing new tools and services to the debt management space. For debt consolidation 2026, expect to see:

- AI-Powered Financial Advisors: More sophisticated AI tools will help individuals analyze their debt, compare consolidation options, and even predict optimal repayment strategies.

- Personalized Loan Offers: Lenders will use advanced algorithms to offer highly personalized interest rates and terms based on a more holistic view of an applicant’s financial health, beyond just credit scores.

- Blockchain for Transparency: While still nascent, blockchain technology could introduce greater transparency and security in lending and debt management processes.

- Increased Focus on Financial Wellness: More financial institutions and employers will offer comprehensive financial wellness programs that include debt consolidation as a key component.

Case Study: Sarah’s Journey to 12% Interest Reduction with Debt Consolidation 2026

Let’s consider Sarah, a fictional individual in mid-2025, burdened with multiple high-interest debts:

- Credit Card 1: $8,000 at 24% APR

- Credit Card 2: $5,000 at 22% APR

- Personal Loan (old): $7,000 at 18% APR

- Total Debt: $20,000

- Weighted Average APR: Approximately 21.5%

Sarah’s credit score was 710. She decided to pursue debt consolidation 2026. After researching and applying to several lenders, she qualified for a personal loan of $20,000 at a fixed APR of 9.5% over a 5-year term. She also chose a lender with no origination fee.

Result: Sarah reduced her weighted average interest rate from 21.5% to 9.5%, a substantial reduction of 12%. This translated into significant monthly savings and a clear path to becoming debt-free. She committed to her repayment plan and avoided new debt, successfully leveraging debt consolidation 2026 for her financial benefit.

Steps to Take Today for Smart Debt Consolidation in 2026

If you’re considering debt consolidation 2026, here’s a roadmap to get started:

- Audit Your Debts: List every debt, its balance, interest rate, and minimum payment.

- Check Your Credit Score: Obtain your credit report and score from all three major bureaus (Equifax, Experian, TransUnion). Look for errors and dispute them.

- Set a Realistic Budget: Understand your income and expenses to determine how much you can comfortably afford for a consolidated payment.

- Research Options: Explore balance transfer cards, personal loans, home equity options, and credit counseling agencies.

- Compare Offers: Don’t settle for the first offer. Compare interest rates, fees, and terms from multiple providers.

- Apply Strategically: Once you’ve chosen the best option, apply. Be prepared with necessary documentation (ID, proof of income, debt statements).

- Implement Your Repayment Plan: Once approved, consolidate your debts and commit to your new payment schedule.

- Monitor Your Progress: Regularly review your finances and celebrate milestones as you pay down your consolidated debt.

Conclusion: Empowering Your Financial Future with Smart Debt Consolidation 2026

Debt consolidation 2026 offers a powerful pathway to financial freedom by simplifying your debts and significantly reducing interest payments. Whether through balance transfer cards, personal loans, home equity products, or a debt management plan, the key is to choose the strategy that best fits your individual circumstances and to execute it with discipline. By taking proactive steps, improving your credit, and diligently comparing options, you can achieve a remarkable reduction in your loan interest, potentially by 10% or more, and pave the way for a more stable and prosperous financial future in 2026 and beyond. Don’t let high-interest debt hold you back; embrace smart consolidation and take control of your financial destiny.