Mastering Your Money: Budgeting for Inflation in 2026

Anúncios

Mastering Your Money: Budgeting for Inflation in 2026

As we look ahead to 2026, the specter of inflation continues to loom large over personal finances worldwide. The purchasing power of our money is under constant threat, making proactive and intelligent budgeting for inflation not just a recommendation, but a necessity. This comprehensive guide will equip you with the knowledge and strategies to navigate the economic landscape of 2026, ensuring your financial stability and growth.

Anúncios

Understanding inflation’s impact is the first step toward mitigating its effects. Inflation erodes the value of currency over time, meaning that the same amount of money buys less today than it did yesterday, and will buy even less tomorrow. For individuals and families, this translates into higher costs for everyday necessities, from groceries and fuel to housing and healthcare. Without a strategic approach, your carefully crafted budget can quickly become obsolete, leaving you struggling to meet your financial goals.

The year 2026 presents its own unique set of economic challenges and opportunities. Global supply chain issues, geopolitical tensions, and shifting consumer demands all contribute to an unpredictable inflationary environment. Therefore, adapting your personal budget to account for these variables is crucial. This article will delve deep into practical steps you can take to adjust your spending habits, optimize your savings, and explore investment opportunities that offer protection against rising costs.

Anúncios

Our goal is to empower you with actionable insights, transforming uncertainty into confidence. By the end of this read, you will have a clear roadmap to not just survive, but thrive financially in 2026, regardless of the inflationary pressures that may arise. Let’s embark on this journey to strengthen your financial future together.

Understanding the Dynamics of Inflation in 2026

Before we can effectively implement budgeting for inflation strategies, it’s vital to grasp the underlying economic forces at play. Inflation isn’t a monolithic phenomenon; it’s influenced by a complex interplay of factors that can shift rapidly. In 2026, we can anticipate several key drivers that will likely continue to shape the inflationary environment.

One primary factor is global supply chain resilience. The disruptions experienced in recent years have highlighted vulnerabilities that can lead to significant price increases. If these supply chains remain fragile, or if new geopolitical events cause further interruptions, the cost of goods and services will likely continue to climb. This directly impacts everything from the cost of manufacturing to the price you pay for items on store shelves.

Another significant driver is energy prices. Fluctuations in oil and gas markets have a ripple effect across the entire economy, impacting transportation costs for goods, utility bills for homes and businesses, and even the cost of producing food. Forecasting energy prices is notoriously difficult, but remaining aware of global energy trends will be essential for anticipating inflationary pressures.

Wage growth and labor markets also play a crucial role. While rising wages can be beneficial for individual incomes, if they outpace productivity growth, they can contribute to cost-push inflation, where businesses pass on higher labor costs to consumers through increased prices. Monitoring unemployment rates and average wage increases can offer clues about the direction of inflation.

Government policies, including fiscal spending and monetary decisions by central banks, are equally impactful. Large government spending programs, especially if not matched by increased production, can inject more money into the economy, potentially leading to demand-pull inflation. Conversely, central banks’ interest rate hikes are a common tool to combat inflation by cooling down economic activity, but these can also affect borrowing costs and economic growth.

Technological advancements and their adoption rates can also influence inflationary trends. While technology often drives efficiency and lowers costs in the long run, initial investment in new technologies can sometimes lead to temporary price increases. Furthermore, the increasing reliance on digital services and infrastructure could introduce new cost structures that impact various sectors.

Finally, consumer behavior itself is a powerful force. Anticipation of rising prices can lead to increased spending in the short term, fueling demand and pushing prices even higher. Conversely, if consumers become more cautious, demand can soften, potentially easing inflationary pressures. Understanding these dynamics is the bedrock upon which effective budgeting for inflation must be built.

Assessing Your Current Financial Health for 2026

Before you can adjust your budget for 2026, you need a clear, honest assessment of your current financial health. This involves more than just looking at your bank balance; it requires a deep dive into your income, expenses, assets, and liabilities. This foundational step is critical for developing a realistic and effective inflation-proof budget.

Detailed Income and Expense Analysis

Start by meticulously tracking your income and expenses for at least three to six months. This will give you an accurate picture of where your money is truly going. Categorize every expenditure, from fixed costs like rent or mortgage payments to variable costs like groceries, entertainment, and transportation. Don’t forget those often-overlooked subscriptions or occasional purchases that add up over time.

- Fixed Expenses: These are generally stable, such as rent, mortgage, loan payments, and insurance premiums.

- Variable Expenses: These fluctuate, including groceries, utilities (which can become semi-variable with inflation), dining out, entertainment, and personal care.

- Discretionary Spending: Items you can cut back on if needed, like vacations, luxury goods, or excessive entertainment.

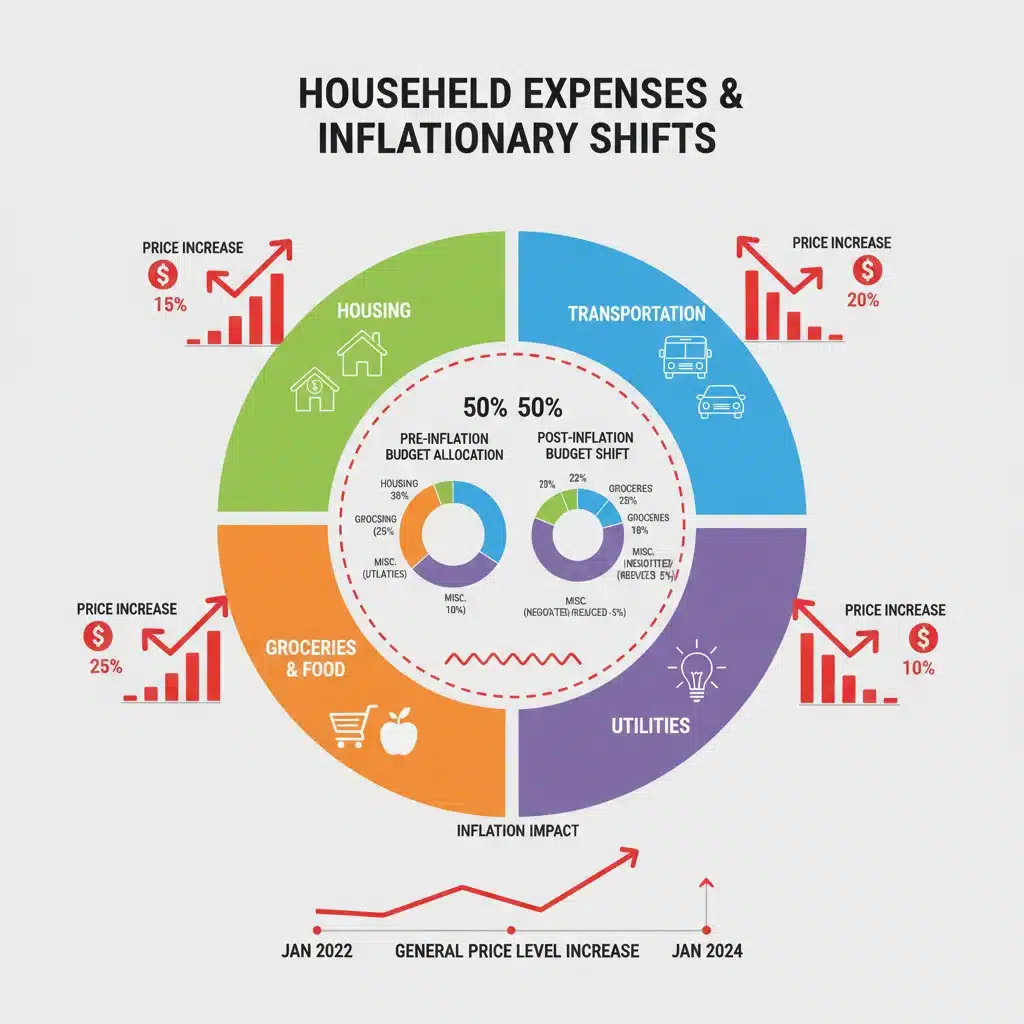

Pay special attention to areas where you anticipate significant inflation-driven price increases. For instance, food prices and energy costs are often among the first to rise. Your historical data will serve as a baseline against which you can project future inflationary impacts.

Reviewing Your Assets and Liabilities

Beyond your cash flow, a complete financial health check includes an inventory of your assets and liabilities. Assets include savings accounts, investment portfolios, real estate, and other valuable possessions. Liabilities encompass debts such as credit card balances, personal loans, student loans, and mortgages.

Understanding your net worth (assets minus liabilities) provides a snapshot of your overall financial standing. In an inflationary environment, certain assets, like real estate or inflation-protected securities, might perform better than others. Conversely, high-interest debt can become an even greater burden as inflation eats away at your purchasing power.

Emergency Fund Assessment

An adequate emergency fund is paramount in any economic climate, but especially so during periods of inflation. Aim to have at least three to six months’ worth of essential living expenses saved in an easily accessible, liquid account. This fund acts as a buffer against unexpected costs and job loss, preventing you from having to take on high-interest debt when prices are already rising.

Identifying Financial Goals

Finally, revisit your financial goals. Are you saving for a down payment, retirement, a child’s education, or a significant purchase? Inflation can significantly alter the real cost of achieving these goals. By re-evaluating them now, you can adjust your savings targets and strategies to ensure your money retains its value and you stay on track.

This thorough assessment forms the foundation for effective budgeting for inflation. Without knowing where you stand, it’s impossible to chart a course forward.

Key Strategies for Adjusting Your Personal Budget in 2026

Once you have a clear picture of your financial health, it’s time to implement concrete strategies for budgeting for inflation in 2026. These adjustments will help you maintain your purchasing power and achieve your financial goals despite rising costs.

1. Re-evaluating and Prioritizing Expenses

Go through your detailed expense analysis and identify areas where you can cut back. This isn’t about deprivation, but about making conscious choices. Differentiate between needs, wants, and luxuries.

- Needs: Housing, food, essential utilities, transportation for work, basic healthcare.

- Wants: Dining out, entertainment subscriptions, new gadgets, certain clothing items.

- Luxuries: High-end purchases, frequent travel, extravagant hobbies.

Consider reducing or eliminating discretionary spending. Can you cook more meals at home instead of eating out? Are there subscriptions you no longer use? Can you find cheaper alternatives for certain services? Even small cuts can add up significantly over a year.

2. Optimizing Your Grocery Budget

Food prices are often a major contributor to inflationary strain. Smart grocery shopping can yield substantial savings.

- Meal Planning: Plan your meals for the week to create a precise shopping list and avoid impulse buys.

- Bulk Buying (Wisely): Purchase non-perishable goods in bulk when prices are low, but ensure you have storage and will use them before they expire.

- Shop Sales and Use Coupons: Take advantage of weekly specials and digital coupons.

- Store Brands: Often, store brands offer comparable quality to name brands at a fraction of the cost.

- Reduce Food Waste: Leftovers can be repurposed, and proper storage can extend the life of produce.

3. Managing Transportation Costs

Fuel prices are notoriously volatile. Look for ways to reduce your reliance on personal vehicles.

- Public Transport/Carpooling: Explore alternatives for commuting.

- Combine Errands: Group your trips to reduce driving time.

- Vehicle Maintenance: Keep your car well-maintained for optimal fuel efficiency.

- Walking/Cycling: For shorter distances, these are healthy and free options.

4. Controlling Utility Expenses

Energy costs are another area hit hard by inflation. Small changes can make a big difference.

- Energy-Efficient Appliances: If possible, invest in appliances with Energy Star ratings.

- Smart Thermostats: Program your heating and cooling to optimize energy use.

- Insulation and Weatherstripping: Improve your home’s energy efficiency to reduce heating and cooling loss.

- Unplug Electronics: “Phantom load” can add to your electricity bill.

5. Reviewing Housing Costs

Housing is often the largest expense. While major changes might not always be possible, consider:

- Refinancing: If interest rates are favorable, refinancing your mortgage could lower monthly payments.

- Negotiating Rent: For renters, a polite negotiation with your landlord might yield a stable rate or smaller increase.

- Downsizing/Roommates: More drastic measures, but worth considering if housing costs become unsustainable.

6. Boosting Your Income

Increasing your income is a powerful counter-inflationary strategy. This could involve:

- Negotiating a Raise: Present a strong case for why you deserve higher compensation based on your contributions and market value.

- Side Hustles: Explore freelancing, consulting, or part-time work to supplement your main income.

- Monetizing Hobbies: Turn a passion into a source of income.

7. Debt Management in an Inflationary Environment

High-interest debt becomes even more burdensome during inflation. Prioritize paying off credit card debt and other variable-rate loans. Consider debt consolidation or balance transfers to lower interest rates if possible. The less you pay in interest, the more money you have to combat rising costs.

By systematically applying these strategies, you can build a resilient personal budget that withstands the pressures of inflation in 2026 and beyond. The key is consistency and a willingness to adapt.

Smart Saving and Investment Strategies Against Inflation

While adjusting your spending is crucial, equally important is ensuring your savings and investments are working effectively to combat inflation. Simply letting money sit in a standard savings account will likely lead to a loss of purchasing power. This section focuses on smart saving and investment strategies for effective budgeting for inflation in 2026.

Protecting Your Savings

Traditional savings accounts often offer interest rates below the rate of inflation, meaning your money loses value over time. Consider these alternatives:

- High-Yield Savings Accounts: While still potentially below inflation, these offer better returns than standard accounts.

- Certificates of Deposit (CDs): CDs lock in your money for a set period in exchange for a fixed interest rate, which can sometimes be higher than savings accounts.

- I-Bonds (Inflation-Protected Savings Bonds): These U.S. Treasury bonds offer a composite interest rate that adjusts with inflation, making them an excellent option for protecting purchasing power, especially for emergency funds or short-to-medium term savings.

Investing for Growth and Inflation Protection

To truly outpace inflation, you’ll likely need to invest. Here are investment avenues often considered good hedges against inflation:

- Real Estate: Historically, real estate has been a strong inflation hedge. Property values and rental income tend to rise with inflation, providing both capital appreciation and passive income. Consider direct ownership, REITs (Real Estate Investment Trusts), or even crowdfunding platforms.

- Stocks (Equities): Companies with strong pricing power – those that can pass on increased costs to consumers without losing significant market share – tend to perform well during inflationary periods. Focus on companies in essential sectors, those with strong brands, or those with low debt. Dividend-paying stocks can also provide a steady income stream.

- Treasury Inflation-Protected Securities (TIPS): Like I-Bonds, TIPS are government bonds whose principal value adjusts with the Consumer Price Index (CPI), offering direct protection against inflation.

- Commodities: Assets like gold, silver, oil, and other raw materials often see their prices rise during inflation. While they can be volatile, a small allocation to commodities can diversify your portfolio and provide a hedge.

- Diversified Portfolio: The most robust strategy is a well-diversified portfolio that includes a mix of these assets. Diversification helps spread risk and capture growth opportunities across different market conditions. Regularly rebalance your portfolio to ensure it remains aligned with your risk tolerance and financial goals.

Reviewing Your Retirement Accounts

Don’t overlook your 401(k)s, IRAs, and other retirement vehicles. Ensure your chosen funds within these accounts are aligned with your inflation-hedging strategy. Many target-date funds automatically adjust their asset allocation over time, but it’s wise to review their underlying holdings to confirm they offer adequate protection against rising costs, especially as you approach retirement.

Seeking Professional Advice

Navigating the complexities of inflation and investment can be challenging. Consider consulting a qualified financial advisor who can help you tailor a personalized investment strategy that aligns with your risk tolerance, time horizon, and financial goals, specifically considering the inflationary outlook for 2026.

By combining smart saving techniques with strategic investments, you can build a financial fortress that not only withstands inflation but also helps your wealth grow over time. This proactive approach to budgeting for inflation is key to long-term financial security.

Technology and Tools for Effective Inflation Budgeting

In the digital age, managing your finances and adapting your budget to inflation is made significantly easier with the right technology and tools. These resources can help you track spending, monitor inflation, and make informed decisions about your budgeting for inflation strategies in 2026.

Budgeting Apps and Software

Gone are the days of manual ledger books. Modern budgeting apps offer powerful features to help you categorize expenses, set spending limits, and visualize your financial flow. Many can sync directly with your bank accounts and credit cards, automating much of the data entry.

- Mint: A popular free app that tracks spending, creates budgets, and monitors your credit score.

- YNAB (You Need A Budget): Known for its “zero-based budgeting” philosophy, YNAB helps you give every dollar a job, which is particularly effective when managing tighter budgets due to inflation.

- Personal Capital: Offers comprehensive financial tracking, including investments, and provides tools for net worth analysis and retirement planning.

- Excel/Google Sheets: For those who prefer a hands-on approach, spreadsheets offer unparalleled flexibility to create custom budgeting templates tailored to your specific needs.

These tools provide real-time insights, allowing you to quickly identify areas where inflation is hitting hardest and adjust your spending accordingly.

Inflation Trackers and Economic Data Sources

Staying informed about economic trends is crucial. Several resources provide up-to-date inflation data and economic forecasts:

- Bureau of Labor Statistics (BLS): For U.S. data, the BLS provides detailed Consumer Price Index (CPI) reports, which are the primary measure of inflation.

- Federal Reserve Economic Data (FRED): A vast database of economic statistics, including various inflation measures, interest rates, and employment data.

- Reputable Financial News Outlets: Major financial news sources (e.g., The Wall Street Journal, Bloomberg, Reuters) offer expert analysis and commentary on economic conditions and inflation outlooks.

- Economic Research Websites: Many financial institutions and academic bodies publish research and forecasts on inflation and economic growth.

Regularly checking these sources will help you anticipate changes and proactively adapt your personal budget before they significantly impact your finances.

Investment Tracking and Management Platforms

For your investment strategies, specialized platforms can help you monitor performance, rebalance your portfolio, and identify opportunities.

- Brokerage Platforms: Most online brokers (e.g., Fidelity, Schwab, Vanguard) offer robust tools for tracking your investments, analyzing performance, and executing trades.

- Robo-Advisors: Services like Betterment or Wealthfront use algorithms to manage diversified portfolios, often with an emphasis on low-cost ETFs, which can be a good option for inflation hedging. They can also automatically rebalance your portfolio.

- Portfolio Trackers: Tools like Morningstar or Yahoo Finance allow you to input your holdings and get consolidated views of your portfolio’s performance and asset allocation.

Comparison Shopping Apps and Websites

To combat rising prices on everyday goods, leverage comparison shopping tools:

- Google Shopping: Quickly compare prices across multiple retailers.

- Price Tracking Extensions: Browser extensions like Honey or CamelCamelCamel (for Amazon) track historical prices and alert you to drops, helping you buy at the lowest possible cost.

- Grocery Store Apps: Many supermarkets offer their own apps with digital coupons, weekly ads, and loyalty programs.

By integrating these technologies into your financial routine, you can gain greater control, make more informed decisions, and enhance the effectiveness of your budgeting for inflation efforts in 2026. The goal is to automate as much as possible, freeing up your time to focus on strategic adjustments rather than manual tracking.

Long-Term Financial Planning Beyond 2026

While our focus has been on budgeting for inflation specifically for 2026, true financial resilience requires a long-term perspective. Inflation is not a one-time event; it’s a persistent economic force that demands ongoing attention. Developing a long-term financial plan that incorporates inflation protection is paramount for securing your future.

Regular Budget Reviews and Adjustments

Inflationary pressures won’t disappear after 2026. Make it a habit to review and adjust your budget quarterly or at least semi-annually. This allows you to account for ongoing price changes, shifts in your income or expenses, and evolving financial goals. A dynamic budget is a powerful tool against the erosion of purchasing power.

Continuous Learning and Adaptation

The economic landscape is constantly evolving. Stay informed about global and local economic trends, monetary policy changes, and emerging investment opportunities. The more knowledgeable you are, the better equipped you’ll be to adapt your financial strategies and protect your wealth. Financial literacy is an ongoing journey, not a destination.

Diversifying Income Streams

Relying on a single source of income can be risky, especially during economic uncertainty. Over the long term, explore ways to diversify your income streams. This could involve developing new skills for a side hustle, investing in dividend-paying stocks, or generating passive income from rental properties or intellectual property. Multiple income streams provide a buffer against job loss or stagnant wages.

Investing in Yourself

One of the best long-term hedges against inflation is investing in your human capital. Acquire new skills, pursue further education, or seek certifications that increase your earning potential. As the cost of living rises, so too should your ability to command a higher salary or generate more income. This personal growth directly translates into greater financial stability.

Building a Strong Financial Foundation

Ensure you have a robust financial foundation that includes:

- Adequate Emergency Fund: Maintain at least 6-12 months of living expenses in a high-yield savings account or inflation-protected securities.

- Reduced Debt Burden: Strategically pay down high-interest debt to free up cash flow and reduce financial vulnerability.

- Comprehensive Insurance Coverage: Protect your assets and income with appropriate health, life, disability, home, and auto insurance. Unexpected events can derail even the best financial plans.

Estate Planning and Legacy

As you build wealth and plan for the long term, don’t overlook estate planning. A well-structured estate plan ensures your assets are distributed according to your wishes and can minimize tax implications for your heirs. While not directly related to inflation, it’s a critical component of a comprehensive long-term financial strategy.

Automating Savings and Investments

Set up automatic transfers to your savings and investment accounts. This “pay yourself first” approach ensures you consistently contribute to your financial goals, even when faced with rising costs. Automation removes the temptation to spend money that should be saved or invested.

By integrating these long-term planning principles with your immediate budgeting for inflation strategies for 2026, you can create a sustainable path to financial security and prosperity that transcends short-term economic fluctuations. The key is consistent effort, informed decision-making, and a commitment to your financial well-being.

Conclusion: Your Resilient Financial Future in an Inflationary World

Navigating the economic landscape of 2026, characterized by ongoing inflationary pressures, demands a proactive and informed approach to personal finance. The journey of budgeting for inflation is not merely about cutting costs; it’s about strategically managing your money to preserve and grow your purchasing power, ensuring your financial goals remain within reach.

We’ve explored the complex dynamics of inflation, emphasizing the need to understand its drivers to anticipate its impact. We then delved into the crucial step of assessing your current financial health, laying the groundwork for targeted adjustments. From there, we outlined a comprehensive set of strategies for adapting your personal budget, focusing on smart spending, optimizing essential expenses, and identifying opportunities to boost your income.

Beyond immediate budgetary adjustments, we highlighted the importance of smart saving and investment strategies. Protecting your savings through high-yield accounts and inflation-protected bonds, and investing for growth in assets like real estate, equities, and commodities, are vital components of an inflation-resilient financial plan. These steps ensure your money isn’t just sitting idle but actively working to counteract the effects of rising prices.

Furthermore, we acknowledged the invaluable role of technology and tools in modern financial management. Budgeting apps, inflation trackers, and investment platforms empower you with real-time data and automation, making the process of adapting your budget more efficient and effective. Leveraging these resources can transform a daunting task into a manageable routine.

Finally, we looked beyond 2026, stressing that true financial mastery is a long-term endeavor. Regular budget reviews, continuous learning, income diversification, and investing in yourself are all pillars of enduring financial resilience. By building a strong financial foundation and maintaining a forward-looking perspective, you can navigate not just the challenges of 2026 but also any future economic uncertainties.

The path to a resilient financial future in an inflationary world is paved with knowledge, discipline, and adaptability. By implementing the strategies outlined in this guide, you are not just reacting to inflation; you are actively shaping your financial destiny. Take control, make informed decisions, and build a secure and prosperous future for yourself and your loved ones. Your journey to mastering budgeting for inflation starts now.