Credit Score Improvement 2026: Boost Your Score by 50 Points in 6 Months

Anúncios

Credit Score Improvement 2026: Boost Your Score by 50 Points in 6 Months

Are you looking to achieve significant credit score improvement in 2026? A strong credit score is more than just a number; it’s a gateway to better financial opportunities, from securing favorable loan rates to renting an apartment or even getting a new job. In today’s economic climate, having a robust credit profile is more crucial than ever. Many people dream of boosting their credit score, but often feel overwhelmed by the process. The good news is that with a strategic approach and consistent effort, you can see remarkable changes. This comprehensive guide will equip you with 4 actionable steps designed to help you elevate your credit score by a minimum of 50 points within just six months. We’ll delve into the intricacies of credit scoring, debunk common myths, and provide a clear roadmap to financial empowerment.

Anúncios

Understanding your credit score is the first step toward improving it. Your credit score, primarily FICO and VantageScore, is a three-digit number that lenders use to assess your creditworthiness. It reflects your financial behavior and your ability to manage debt responsibly. Factors like payment history, amounts owed, length of credit history, new credit, and credit mix all play a role in determining this crucial number. A higher score signifies lower risk to lenders, translating into better terms and conditions for you. Conversely, a lower score can lead to higher interest rates, stricter loan approvals, and even impact your insurance premiums or job prospects. Therefore, focusing on credit score improvement is not just about getting a loan; it’s about building a solid financial planning foundation for your future.

The year 2026 presents a fresh opportunity to reset and refine your financial habits. With the right strategies, a 50-point increase in six months is not only achievable but often a realistic goal for many individuals. This guide is structured to provide you with practical, easy-to-follow advice that you can implement immediately. We will focus on key areas that have the most significant impact on your credit score, ensuring that your efforts are both efficient and effective. Let’s embark on this journey to remarkable credit score improvement together.

Anúncios

Step 1: Understand Your Credit Report and Score

The foundation of any successful credit score improvement plan begins with a thorough understanding of your current credit standing. This means obtaining and meticulously reviewing your credit reports from all three major credit bureaus: Experian, Equifax, and TransUnion. You are legally entitled to one free report from each bureau annually via AnnualCreditReport.com. Don’t just glance at them; dive deep.

Why Reviewing Your Credit Report is Crucial for Credit Score Improvement

Your credit report is a detailed history of your borrowing and repayment activities. It contains personal information, credit accounts (both open and closed), public records (like bankruptcies), and inquiries. Any inaccuracies or errors on these reports can negatively impact your score, sometimes significantly. Identifying and disputing these errors is a critical first step towards credit score improvement.

- Identify Errors: Look for incorrect account balances, accounts you don’t recognize, duplicate accounts, incorrect payment statuses, or outdated information. Even a misspelled name or incorrect address can sometimes be an indicator of deeper issues.

- Understand Your Payment History: This is the most significant factor in your credit score (35% of your FICO score). Note any late payments, collections, or charge-offs. These can linger on your report for up to seven years, but understanding their presence is vital for future planning.

- Assess Credit Utilization: This refers to the amount of credit you’re using compared to your total available credit. High utilization ratios (typically above 30%) can hurt your score. We’ll discuss this more in Step 3.

- Check for Hard Inquiries: These occur when you apply for new credit and can slightly lower your score for a short period. Too many in a short span can signal higher risk to lenders.

Disputing Inaccuracies: Your Right to a Clean Report

If you find errors, you have the right to dispute them with the credit bureaus. This process is free and relatively straightforward:

- Gather Documentation: Collect any evidence that supports your claim (e.g., payment receipts, bank statements, previous credit reports).

- Contact the Credit Bureaus: You can submit disputes online, by mail, or by phone. Provide clear, concise information about the error and include your supporting documents.

- Notify the Creditor: It’s also a good idea to contact the creditor that reported the incorrect information directly.

- Follow Up: The credit bureaus typically have 30 days to investigate your dispute. Keep records of all correspondence and follow up if you don’t hear back. Successfully removing errors can lead to immediate credit score improvement.

By diligently reviewing your credit reports and correcting any discrepancies, you lay a strong foundation for your credit score improvement journey. This proactive approach ensures that your score accurately reflects your financial behavior, setting the stage for positive changes.

Step 2: Prioritize On-Time Payments and Address Delinquencies

As mentioned, your payment history is the single most influential factor in your credit score, accounting for 35% of your FICO score. Consistently making on-time payments is the most effective way to demonstrate responsible financial behavior and drive significant credit score improvement. Conversely, even a single late payment can have a substantial negative impact, potentially dropping your score by dozens of points.

The Power of Punctual Payments for Credit Score Improvement

Every on-time payment reinforces your creditworthiness. Lenders want to see a consistent pattern of timely repayments, as it indicates reliability. To ensure you never miss a payment:

- Automate Payments: Set up automatic payments from your checking account for all your credit cards, loans, and bills. Even if it’s just the minimum payment, consistency is key. You can often schedule these payments through your bank or directly with the creditor.

- Set Reminders: Use calendar alerts, phone reminders, or budgeting apps to notify you a few days before each payment due date. This provides a backup system for automated payments or allows you to manually pay if automation isn’t possible.

- Align Due Dates: If possible, contact your creditors to adjust your payment due dates to align with your paychecks. This can make managing your finances easier and reduce the risk of accidental late payments.

- Pay More Than the Minimum: While paying the minimum is crucial for avoiding late fees and negative marks, paying more whenever possible will not only save you money on interest but also reduce your credit utilization, which positively contributes to credit score improvement.

Addressing Existing Delinquencies and Collections

If you have past late payments, accounts in collections, or charge-offs, addressing them strategically is vital for credit score improvement. While these negative marks remain on your report for several years, how you handle them can mitigate their impact.

Late Payments:

- Contact the Creditor Immediately: If you’ve just missed a payment, call your creditor right away. Explain your situation and ask if they can waive the late fee or report it as on-time, especially if it’s your first time. Some creditors are willing to work with good customers.

- "Pay for Delete" (for older late payments/collections): For accounts that have gone to collections, you might be able to negotiate a "pay for delete" agreement. This is where you agree to pay a portion or all of the debt in exchange for the collection agency removing the derogatory mark from your credit report. Get any such agreement in writing before making a payment. While not always successful, it’s worth exploring for significant credit score improvement.

Collections and Charge-Offs:

- Validate the Debt: If a collection agency contacts you, first request a debt validation letter. This ensures the debt is legitimate and that they have the right to collect it.

- Negotiate a Settlement: Collection agencies often buy debts for pennies on the dollar, so they may be willing to settle for less than the full amount. Prioritize paying off collections, as they severely damage your score. Once paid, the negative impact lessens over time, even if not removed.

- Avoid New Delinquencies: The most important step is to prevent any new late payments. The older a negative mark is, the less impact it has on your score. New delinquencies, however, will reset the clock on negative reporting and severely hinder your credit score improvement efforts.

By mastering your payment schedule and proactively addressing any existing negative marks, you’ll be tackling the biggest component of your credit score head-on. This dedicated effort will yield substantial gains in your credit score improvement journey over the next six months.

Step 3: Strategically Manage Credit Utilization

Credit utilization is the second most important factor in your credit score, accounting for 30% of your FICO score. It refers to the amount of revolving credit you are currently using compared to your total available revolving credit. For example, if you have a credit card with a $10,000 limit and you owe $3,000, your utilization is 30%. Keeping this ratio low is paramount for significant credit score improvement.

The "Golden Rule" of Credit Utilization for Credit Score Improvement

Experts generally recommend keeping your overall credit utilization below 30%. For optimal credit score improvement, many suggest aiming for even lower, ideally under 10%. The lower your utilization, the more responsible you appear to lenders. Here’s why and how to achieve it:

- Signifies Low Risk: A low utilization ratio indicates that you are not overly reliant on borrowed money and can manage your credit responsibly. High utilization, on the other hand, can suggest financial distress or an inability to manage spending.

- Impact on Score: A sudden spike in utilization can cause a dramatic drop in your credit score, even if you pay on time. Conversely, reducing your utilization can lead to a rapid increase in your score.

Actionable Strategies to Lower Your Credit Utilization

Achieving a low credit utilization ratio doesn’t always mean paying off all your debt at once. Here are practical ways to manage and reduce it for effective credit score improvement:

- Pay Down Balances: This is the most direct way. Focus on paying down your credit card balances, especially those with the highest utilization. If you have multiple cards, prioritize the one closest to its limit.

- Make Multiple Payments Per Month: Instead of waiting for the statement due date, make smaller payments throughout the month. This can keep your reported balance lower to the credit bureaus, as they often report the balance on your statement closing date. This can lead to immediate credit score improvement.

- Increase Your Credit Limit: If you have a good payment history and a stable income, you can request a credit limit increase on an existing card. This increases your total available credit, which in turn lowers your utilization ratio, assuming your spending doesn’t increase proportionally. Be cautious with this strategy; only do it if you trust yourself not to spend more.

- Open a New Credit Line (Carefully): Opening a new credit card can also increase your total available credit, thereby lowering your utilization. However, this strategy comes with caveats:

- Hard Inquiry: A new application will result in a hard inquiry, which can temporarily ding your score (usually by a few points for a few months).

- Average Age of Accounts: A new account will lower your average age of accounts, another factor in your score.

- Only if Responsible: Only pursue this if you are confident you can manage the new credit responsibly and avoid accumulating more debt. This is generally a long-term strategy and should be approached with caution in the short-term credit score improvement goal.

- Become an Authorized User: If a trusted family member or friend with excellent credit management (low utilization and long history) adds you as an authorized user to one of their credit cards, their positive account history can appear on your credit report, boosting your available credit and potentially lowering your utilization. Ensure they maintain low balances and pay on time.

By actively managing your credit utilization, you are directly influencing a major component of your credit score. Consistent effort in keeping your balances low relative to your limits will yield substantial credit score improvement within the six-month timeframe.

Step 4: Diversify Your Credit Mix and Build Credit History

While payment history and credit utilization are the heavy hitters, the length of your credit history and your credit mix also contribute to your score (15% and 10% respectively for FICO). Focusing on these areas, especially as you work on the more impactful factors, can further solidify your credit score improvement.

Length of Credit History: Patience is a Virtue for Credit Score Improvement

Lenders prefer to see a long history of responsible credit use. The longer your accounts have been open and in good standing, the better. This factor is largely time-dependent, but you can adopt habits to protect it:

- Don’t Close Old Accounts: Unless an old account has an annual fee you can’t justify, or you have a strong reason to close it (e.g., an account that encourages irresponsible spending), it’s generally best to keep older credit card accounts open, even if you rarely use them. Closing an old account reduces your average age of accounts and decreases your total available credit, potentially harming your utilization ratio and slowing down your credit score improvement.

- Maintain Active Accounts: Use your older credit cards periodically for small purchases and pay them off immediately. This keeps the accounts active and ensures they continue to report positive payment history.

Credit Mix: A Balanced Portfolio for Optimal Credit Score Improvement

Having a healthy mix of different types of credit (revolving credit like credit cards, and installment credit like mortgages, auto loans, or student loans) demonstrates your ability to manage various forms of debt. While you shouldn’t take on debt solely to improve your credit mix, if you’re already considering a loan, understanding its impact is beneficial.

Strategies to Improve Your Credit Mix and History:

- Secured Credit Cards: If you have limited or poor credit, a secured credit card can be an excellent tool for credit score improvement. You provide a cash deposit that acts as your credit limit. This card behaves like a regular credit card, reporting your payments to the bureaus. After consistent on-time payments, many secured cards can transition to unsecured cards.

- Credit-Builder Loans: These are specifically designed to help people establish or rebuild credit. The loan amount is held in a locked savings account while you make regular payments. Once the loan is paid off, you get access to the funds. These loans report to credit bureaus, building positive payment history for credit score improvement.

- Authorized User Status (Revisited): As mentioned in Step 3, being an authorized user on someone else’s well-managed credit card can add their positive payment history and credit limit to your report, contributing to both your credit mix and history.

- Experian Boost and UltraFICO: These programs can help incorporate non-traditional payment history (like utility bills, cell phone bills, and even rent payments) into your Experian or FICO score calculations. While not a substitute for traditional credit, they can offer a quick boost for those with thin credit files, potentially leading to immediate credit score improvement.

- Responsible Installment Loans: If you genuinely need a car loan or student loan, managing these responsibly will add a positive installment account to your credit mix, which can be good for your score over the long term. Remember, the goal is not to take on unnecessary debt.

Building a diverse and long credit history takes time, but by implementing these strategies, you can actively shape this aspect of your credit profile. Combining these efforts with diligent payment practices and smart utilization management will accelerate your credit score improvement substantially within the six-month period and beyond.

Beyond the 6 Months: Sustaining Your Credit Score Improvement

Achieving a 50-point credit score improvement in six months is an excellent milestone, but the journey doesn’t end there. Maintaining and further enhancing your credit score requires ongoing vigilance and commitment to good financial habits. Think of it as a marathon, not a sprint. The strategies you’ve implemented to reach your initial goal are precisely the habits you’ll need to continue to cultivate for long-term financial health.

Continuous Monitoring and Adjustment

Regularly monitoring your credit reports and scores should become a routine practice. While you get free annual reports from each bureau, many credit card companies and financial institutions now offer free credit score tracking services. Utilize these tools to keep an eye on any changes, identify potential issues early, and ensure your credit score improvement remains on track. If you notice a dip, revisit the four steps outlined above to pinpoint the cause and take corrective action.

Budgeting and Debt Management for Ongoing Credit Score Improvement

A well-structured budget is the bedrock of responsible financial management. It allows you to track your income and expenses, identify areas for savings, and allocate funds specifically for debt repayment. By consistently adhering to a budget, you can ensure that you always have enough money to make on-time payments and proactively reduce your credit card balances, thereby maintaining a low credit utilization ratio. Consider using budgeting apps or spreadsheets to simplify this process.

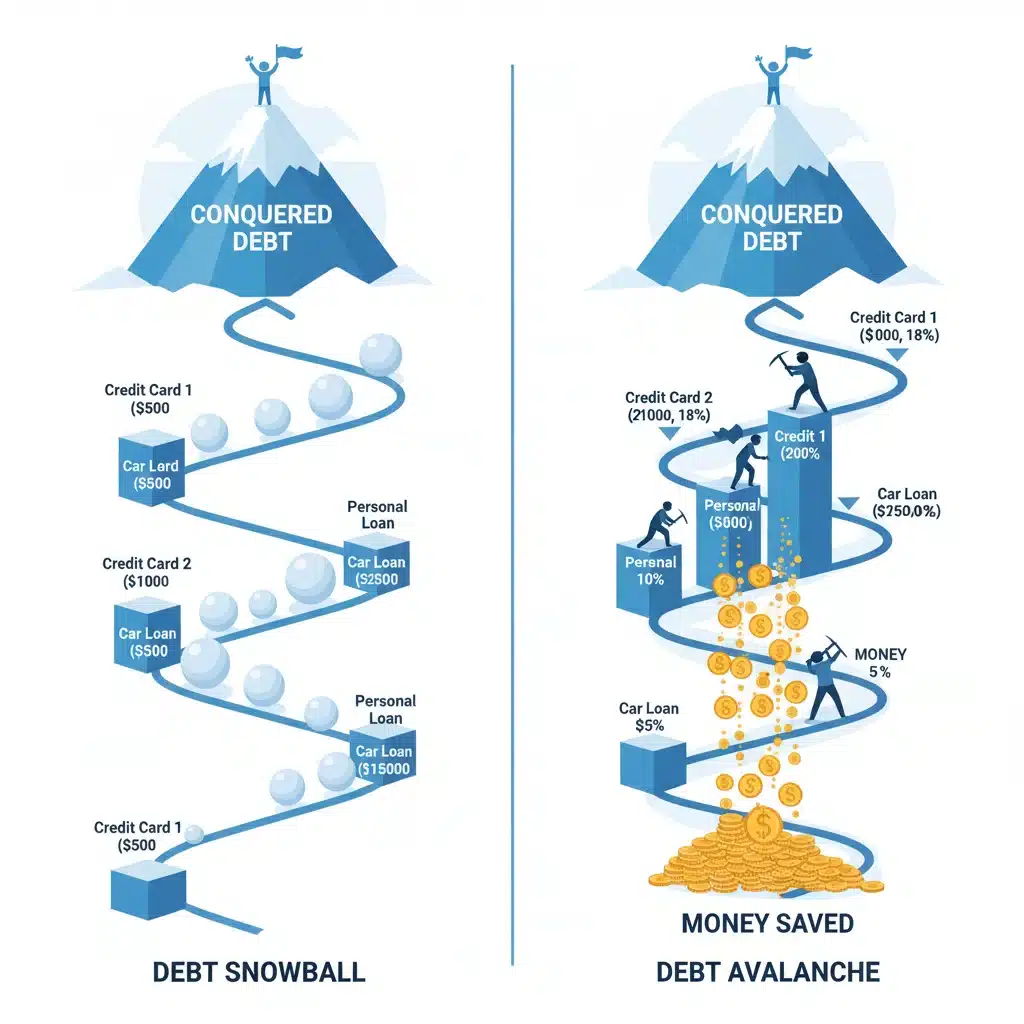

For existing debts, continue to employ smart repayment strategies. If you have multiple credit cards or loans, consider the debt snowball or debt avalanche methods. The debt snowball involves paying off the smallest debt first to gain momentum, while the debt avalanche prioritizes debts with the highest interest rates to save money over time. Both methods can be highly effective in reducing your overall debt burden, which is crucial for sustained credit score improvement.

Strategic Use of Credit

As your credit score improves, you might be tempted to apply for new credit cards or loans. While new credit can be beneficial for your credit mix and overall available credit, it must be approached strategically. Avoid opening too many new accounts in a short period, as this can lead to multiple hard inquiries and a decrease in your average age of accounts, temporarily hindering your credit score improvement. Only apply for credit when you genuinely need it and are confident you can manage the repayments responsibly.

Furthermore, continue to use your credit cards responsibly. Make small purchases and pay them off in full each month to avoid interest charges and maintain a perfect payment history. This demonstrates consistent positive credit behavior, which is invaluable for long-term credit score improvement.

Building an Emergency Fund

An often-overlooked aspect of credit health is having a robust emergency fund. Unexpected expenses – a car repair, a medical bill, or job loss – can quickly derail your financial plans and force you to rely on credit cards, potentially leading to high utilization and missed payments. By building an emergency fund (ideally 3-6 months of living expenses), you create a financial buffer that protects your credit score from unforeseen circumstances, ensuring your credit score improvement efforts are not undone.

Seeking Professional Advice

If you find yourself struggling despite your best efforts, don’t hesitate to seek professional help. Credit counselors can provide personalized advice, help you create a debt management plan, and negotiate with creditors on your behalf. While some services might come with a fee, the long-term benefits of getting your finances back on track can far outweigh the initial cost. They can also offer insights into advanced strategies for credit score improvement tailored to your specific situation.

Your credit score is a dynamic entity that reflects your financial journey. By consistently applying the principles of on-time payments, low credit utilization, a healthy credit mix, and careful monitoring, you can not only achieve your 50-point credit score improvement goal within six months but also build a strong and resilient financial future for years to come. The effort you put in today will pay dividends in the form of better interest rates, increased financial flexibility, and greater peace of mind tomorrow.

Conclusion: Your Path to Enhanced Credit Score Improvement in 2026

Embarking on a journey of credit score improvement can feel daunting, but as we&rsquove explored, it’s an entirely achievable goal with the right strategies and consistent effort. By focusing on these four actionable steps – understanding your credit report, prioritizing on-time payments, strategically managing credit utilization, and diversifying your credit mix – you are not just aiming for a temporary boost, but building a foundation for lasting financial health in 2026 and beyond.

Remember, a 50-point increase in your credit score within six months is a realistic and powerful objective. This improvement can unlock doors to better interest rates on loans, more favorable terms for mortgages and car loans, and even lower insurance premiums. It signifies to lenders that you are a responsible borrower, translating directly into tangible financial benefits for you.

Your credit score is a reflection of your financial habits, and by consciously adopting these proven strategies, you are taking proactive control of your financial destiny. Start today by pulling your credit reports, identifying areas for improvement, and committing to the disciplined practices outlined in this guide. Every on-time payment, every reduction in credit card balance, and every responsible credit decision contributes to your overall credit score improvement.

Don’t underestimate the power of small, consistent actions. Over six months, these actions compound, leading to the significant credit score increase you desire. Stay persistent, monitor your progress, and celebrate each step forward. Your dedication to credit score improvement will undoubtedly lead to a more secure and prosperous financial future. The time to act is now – take these steps and watch your credit score transform.